How I Navigated Risk When Switching Careers — A Real Talk Guide

Changing careers isn’t just about finding a new job — it’s a financial crossroads. I felt the pressure when I left my stable role to start something new. What if I failed? What if I ran out of savings? Through trial and error, I learned to spot hidden risks early. This is my story of how I built a systematic approach to protect my finances while chasing a dream — and how you can too, without losing sleep. It wasn’t about avoiding risk altogether; it was about understanding it clearly, preparing for the unexpected, and making choices grounded in reality rather than hope alone. The journey reshaped not only my career but also my relationship with money, security, and long-term confidence.

The Moment Everything Changed

It started with a quiet realization during a routine Monday morning meeting. I was seated at the conference table, nodding along as quarterly reports were reviewed, but my mind was elsewhere. For years, I had followed a predictable path — steady promotions, consistent paychecks, health benefits, and the unspoken promise of stability. Yet, despite checking all the boxes of professional success, a growing sense of misalignment gnawed at me. The work no longer sparked curiosity or passion. Instead, it felt like maintenance — keeping systems running, not building anything meaningful. That day, I finally admitted to myself: I wanted out.

Leaving wasn’t impulsive. I had spent months reflecting, journaling, and quietly researching alternative paths. But even with preparation, the decision carried immense weight. My salary covered more than just rent and groceries — it supported insurance, retirement contributions, and a modest lifestyle that allowed breathing room. Stepping away meant giving up that structure, trading certainty for possibility. The fear wasn’t just about failing in a new field; it was about what failure would cost financially. Could I afford several months without income? Would I jeopardize my ability to cover emergencies? These questions didn’t have easy answers, and at first, I had no framework to evaluate them objectively.

What made the transition especially daunting was the lack of a clear roadmap. Friends offered encouragement, but few had walked this path themselves. Online advice tended to swing between two extremes: reckless calls to “follow your passion no matter what” or overly cautious warnings to never leave a secure job. Neither resonated. I needed something in between — a way to honor both my desire for change and my responsibility to protect my financial well-being. That balance became the foundation of my next steps. Without realizing it at the time, I was beginning to build a personal risk management strategy — one that would eventually help me move forward with clarity instead of fear.

Why Risk Feels Invisible at First

When you’re standing on the edge of a major life change, excitement often drowns out caution. The vision of a more fulfilling career, greater autonomy, or creative freedom can feel so compelling that practical concerns fade into the background. This isn’t denial; it’s human nature. Our brains are wired to respond to positive possibilities, especially when we’ve been feeling stuck. But that optimism, while motivating, can also be dangerously misleading. During my transition, I underestimated how easily financial risks could go unnoticed until they became urgent problems.

One of the most common blind spots is cash flow disruption. In a traditional job, income arrives like clockwork — every two weeks or monthly, without variation. When you leave that behind, even temporarily, the rhythm breaks. I assumed my savings would stretch far enough to cover a few months of transition, but I hadn’t accounted for irregular expenses or the psychological tendency to maintain old spending habits. Without a paycheck coming in, even small outflows start to feel significant. A routine car repair, an unexpected medical bill, or simply dining out more often due to disrupted routines can quietly erode a buffer that seemed substantial just weeks before.

Another invisible risk is the loss of employer-provided benefits. While salary is easy to quantify, the value of health insurance, retirement matching, paid time off, and even wellness programs is often overlooked. When I left my position, I had to purchase private health coverage — a cost I had never shouldered directly. The premium was higher than expected, and the deductible meant greater out-of-pocket exposure. Similarly, retirement contributions paused during lean months, creating a gap in long-term savings that would take years to recover. These weren’t surprises in hindsight, but they weren’t part of my initial calculations either.

Timing is another factor that distorts perception. Many people assume that if they plan for a three-month transition, they’ll land on their feet by month four. Reality rarely follows such neat timelines. Job searches take longer, freelance clients take time to build, and new ventures often require more runway than anticipated. The danger lies in treating estimates as guarantees. Without contingency plans, even a modest delay can trigger financial strain. Recognizing these invisible risks wasn’t about fostering fear — it was about restoring balance. Once I began to see them clearly, I could start building safeguards.

Building a Personal Risk Radar

To navigate uncertainty effectively, I realized I needed a structured way to identify potential threats before they became crises. I began developing what I now call a “personal risk radar” — a systematic method for scanning ahead, detecting vulnerabilities, and prioritizing which risks deserved attention. This wasn’t about eliminating every possible problem; it was about moving from reactive worry to proactive planning. The goal was to replace guesswork with insight, so decisions could be based on awareness rather than anxiety.

The first step was mapping out all sources of financial exposure. I created a simple list: fixed expenses (rent, utilities, insurance), variable costs (groceries, transportation, subscriptions), and non-negotiable obligations (debt payments, childcare). Then, I layered in potential income changes — not just the loss of salary, but also the uncertainty of when new income might begin. From there, I added secondary risks: What if I got sick during the transition? What if a family member needed support? What if the market shifted, making my target industry less viable? Each item represented a point where disruption could occur.

Next, I assessed each risk based on two criteria: likelihood and potential impact. Some risks were highly probable but low in consequence — for example, a slight increase in grocery spending due to irregular meal planning. Others were less likely but catastrophic — like a major health issue without adequate coverage. By plotting these on a simple matrix, I could focus my energy where it mattered most. This process helped me avoid getting overwhelmed by every possible “what if” and instead concentrate on the few that could truly derail progress.

One of the most valuable insights came from tracking skill transferability. I evaluated which abilities from my previous role could generate income during the transition — writing, project management, consulting — and how quickly I could monetize them. This wasn’t just about confidence; it was about creating fallback options. Knowing I could take on short-term contract work if needed reduced the pressure to rush into a new career prematurely. The radar wasn’t a static tool — I revisited it monthly, adjusting as circumstances changed. Over time, it became less about fear and more about empowerment, giving me a clearer view of the terrain ahead.

Stress-Testing Your Financial Safety Net

Having savings is one thing; knowing whether they’re sufficient is another. I learned this the hard way when an early income projection fell short by nearly two months. What I thought was a six-month runway turned into four, forcing me to adjust quickly. That experience taught me the importance of stress-testing my financial safety net — putting it through realistic worst-case scenarios to see how long it could truly last. This wasn’t about pessimism; it was about realism. A robust safety net isn’t measured by how much you have saved, but by how long it can sustain you under pressure.

I began by simulating a zero-income period of at least six months — longer than I initially expected to need. I reviewed my expense breakdown and separated essentials from discretionary spending. Essentials included housing, basic utilities, food, insurance, and minimum debt payments. Discretionary items — dining out, travel, subscriptions, non-urgent repairs — were marked for reduction or elimination if necessary. This exercise revealed that I could extend my runway by nearly 40% simply by tightening non-essential spending. More importantly, it gave me a concrete plan for action if income stalled.

But financial resilience isn’t only about money. I also evaluated non-monetary supports — my professional network, available skills, and access to part-time opportunities. These elements don’t show up on a balance sheet, but they contribute significantly to stability. For instance, knowing I could reach out to former colleagues for contract work or tap into industry groups for leads made me feel less isolated. I also assessed my adaptability: Could I pivot to a related role if my preferred path didn’t open up? Was my resume flexible enough to appeal to multiple sectors? These questions helped me see my safety net as multidimensional — not just a dollar amount, but a combination of resources, relationships, and readiness.

I also reviewed insurance coverage thoroughly. Beyond health, I considered disability and liability protection, especially since I was exploring self-employment. A single injury or legal issue could wipe out savings fast. While these policies added to monthly costs, they provided critical protection. Stress-testing wasn’t a one-time task; I repeated it quarterly, updating assumptions as my situation evolved. Each round strengthened my confidence, not because risks disappeared, but because I knew I had thought them through.

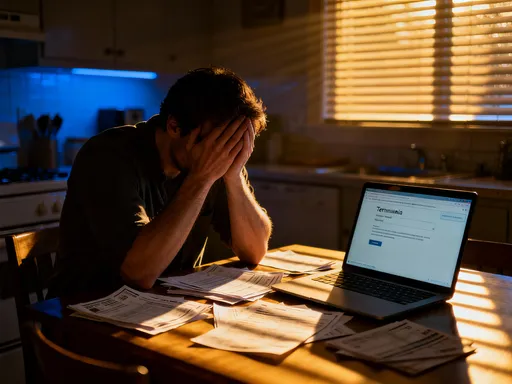

Income Gaps Don’t Happen Overnight — But They Hurt Fast

One of the most underestimated challenges in career switching is the gap between leaving one role and establishing a stable income in another. It’s rarely a clean handoff. Even with careful planning, delays accumulate — applications take longer to process, clients take time to onboard, or certification processes stretch beyond estimates. What starts as a short pause can turn into a prolonged stretch of financial uncertainty. I discovered that while income gaps grow slowly, their impact hits quickly, affecting not just budgets but credit, confidence, and long-term goals.

During my transition, I experienced a four-month gap before earning consistent income in my new field. The first month felt manageable — I was energized by the change and careful with spending. By month three, however, the strain showed. I delayed routine car maintenance, skipped a non-urgent medical check-up, and began relying more on credit for essentials. Small compromises added up, and the psychological toll was real. The constant mental accounting — calculating how many more weeks the savings would last — created background stress that affected sleep and focus.

To shorten future gaps, I adopted a phased approach. Instead of quitting immediately, I explored part-time consulting in my new area while still employed. This allowed me to build experience, earn supplemental income, and test the market demand for my services. I also set milestone-based financial checkpoints — for example, not leaving my job until I had three freelance clients confirmed or until I completed a key certification that increased my earning potential. These markers provided objective criteria for progression, reducing emotional decision-making.

Another effective strategy was creating multiple income entry points. Rather than relying on one path — such as landing a full-time role or launching a business — I diversified. I offered workshops, wrote articles, and took on project-based work. This not only accelerated income generation but also expanded my network and credibility. Each small win built momentum. Over time, I learned that consistency matters more than size — a steady stream of smaller earnings often provides more stability than waiting for one large opportunity. Planning for income gaps isn’t about expecting failure; it’s about ensuring that the journey itself remains sustainable.

The Hidden Costs Nobody Warns You About

When planning a career switch, most people focus on lost salary and basic living expenses. Few anticipate the hidden costs that quietly accumulate — fees, investments, and overhead that aren’t part of everyday budgeting. These expenses are rarely discussed in career advice articles, yet they can significantly erode savings if not planned for. I learned this firsthand when launching a freelance practice. What I thought would be a low-cost transition ended up including legal registration, software subscriptions, equipment upgrades, and professional development — none of which I had fully accounted for in my initial budget.

One of the first surprises was the cost of setting up as a legal entity. To protect myself and appear credible to clients, I registered as a sole proprietorship and later considered an LLC. Filing fees, annual renewals, and accounting support added hundreds of dollars to my first-year expenses. Then came technology needs — a reliable laptop, backup systems, cybersecurity tools, and collaboration software. While some items were one-time purchases, others required ongoing subscriptions. What seemed minor individually — $15 here, $30 there — totaled over $600 per year, a figure that would have strained my budget during lean months.

Taxes were another major blind spot. As an employee, taxes were automatically withheld. As a self-employed individual, I became responsible for estimated quarterly payments, including both income tax and self-employment tax. Failing to set aside funds led to a stressful tax season where I owed more than expected. I also discovered that certain deductions — home office expenses, mileage, professional memberships — required meticulous record-keeping, which I hadn’t prepared for. Hiring a tax professional added further cost but proved necessary to avoid mistakes.

Professional development was another area where investment was unavoidable. To stay competitive, I needed training, certifications, and access to industry events — all of which came with fees, travel costs, and time away from billable work. While these investments paid off in the long run, they created short-term cash flow pressure. The lesson was clear: research matters. I began talking to others who had made similar transitions, asking specifically about unexpected expenses. Their insights helped me create a more accurate financial model. Today, I recommend building a “hidden cost buffer” — an additional 15–20% on top of basic living expenses — to cover these often-overlooked outflows.

Staying Smart Without Stopping Progress

Navigating a career change doesn’t require eliminating risk — it requires managing it wisely. What I’ve learned is that preparation doesn’t stifle progress; it enables it. The more I understood my financial vulnerabilities, the more confident I felt taking meaningful steps forward. Caution and courage aren’t opposites; they can coexist when decisions are informed by data, reflection, and realistic planning. My transition wasn’t perfect — there were delays, setbacks, and moments of doubt — but because I had systems in place, I never felt out of control.

One of the most profound shifts was in my mindset. Early on, I saw risk as something to fear, a barrier to overcome. Over time, I began to view it as information — a signal to prepare, not to retreat. By identifying potential pitfalls early, stress-testing my resources, and planning for income gaps, I transformed uncertainty into structure. This didn’t guarantee success, but it increased the odds significantly. More importantly, it gave me peace of mind. I could pursue a new path not because I was reckless, but because I was ready.

For anyone considering a career switch, the message isn’t to wait until everything is perfect — that moment may never come. It’s to move forward with eyes open. Build your risk radar. Stress-test your savings. Account for hidden costs. Create fallback options. These actions don’t eliminate risk, but they ensure you’re not navigating blind. The goal isn’t to avoid every bump in the road, but to travel with shock absorbers that keep you moving forward.

In the end, the greatest reward wasn’t just landing in a more fulfilling role — it was the confidence that came from knowing I had prepared well. I didn’t chase my dream blindly; I mapped the terrain, packed the right tools, and adjusted as I went. That balance of vision and vigilance made all the difference. You don’t have to choose between security and fulfillment. With the right approach, you can build both — one thoughtful step at a time.