What I Missed When I Switched Careers — The Hidden Costs Nobody Talks About

Changing careers felt like jumping off a cliff with a dream in one hand and a spreadsheet in the other. I thought I’d calculated everything—savings, resume upgrades, networking events. But within months, I was bleeding money on hidden fees, lost benefits, and emotional burnout. This isn’t just about budgets; it’s about the real cost of reinvention. If you're considering a leap, let me walk you through what I wish I’d known before I took mine. The excitement of starting fresh can blind even the most cautious planners. Passion feels like fuel, but it doesn’t pay the mortgage. And when income slows or stops, the financial cracks appear fast. This story isn’t unique to me—it’s shared by thousands who chase new beginnings without seeing the full financial landscape beneath them.

The Leap Nobody Sees Coming

Career transitions are often romanticized as bold moves toward fulfillment, but behind the inspiration is a complex mix of emotional urgency and financial uncertainty. Many professionals leave stable roles not because they’ve secured something better, but because they can no longer tolerate their current environment. Burnout, lack of growth, or misalignment with personal values become unbearable, prompting a rush toward change. The desire for meaning overrides caution, and decisions are made on momentum rather than method. This emotional momentum can feel empowering, but it often leads to underestimating the time, effort, and cost required to rebuild from scratch.

What many fail to recognize is that switching careers isn’t just a job change—it’s a complete reset. You’re not only learning new skills, but also rebuilding credibility, reputation, and income potential. The illusion of a “fresh start” masks the reality of starting at the bottom again, both professionally and financially. People assume that their experience in one field will easily transfer to another, but in practice, employers often see lateral moves as risky unless there’s clear, relevant proof of capability. This gap in perception creates a period of invisibility, where effort doesn’t immediately translate into opportunity or income.

Additionally, identity plays a powerful role in this decision. For years, individuals define themselves by their titles, industries, and achievements. Stepping away from that identity can trigger a sense of loss, even when the change is voluntary. This internal shift is rarely discussed, yet it affects confidence, negotiation power, and financial decision-making. Without a strong sense of professional identity, people may accept lower-paying roles or undervalue their contributions, accelerating financial strain. The emotional weight of starting over compounds over time, especially when progress feels slow and expenses keep rising.

Upfront Costs That Sneak Up on You

When planning a career switch, most people budget for basics like updated clothing or a new laptop. But the real financial drain comes from a wave of less obvious, yet significant, upfront expenses. Certification programs, professional coaching, resume writing services, and industry-specific software subscriptions often appear essential in the moment, promising faster entry into the new field. These costs, individually, may seem manageable—$200 here, $500 there—but together, they form a hidden tax on transitioners who are already facing income disruption.

The promise of “investing in yourself” is powerful and often necessary, but it can also be exploited by programs that overpromise results. Online courses, bootcamps, and career accelerators market themselves as gateways to high-paying jobs, yet many lack accreditation, job placement guarantees, or measurable outcomes. People enroll hoping for transformation, only to find that completion doesn’t equal qualification in the eyes of employers. Worse, some certifications require renewal fees or continuing education, adding recurring costs to an already tight budget. The emotional pressure to “do something” makes it easy to overspend on tools that deliver minimal return.

Technology upgrades are another silent expense. Moving into fields like digital marketing, data analysis, or freelance design often requires software licenses, cloud storage, or specialized hardware. A monthly subscription for editing software or project management tools might be negligible for someone with steady income, but for someone between paychecks, every dollar counts. Even seemingly minor purchases—like a professional headshot, a domain name for a portfolio website, or a virtual assistant subscription—add up quickly when there’s no incoming cash flow.

And because many of these expenses are framed as “one-time” investments, they’re often justified emotionally even when financially risky. The mindset becomes: “I’m building a new future, so this spending is necessary.” While some investments do pay off, the lack of a clear cost-benefit analysis during a vulnerable transition phase leads to overspending. Without a buffer, these costs can deplete emergency funds before the first paycheck in the new role arrives.

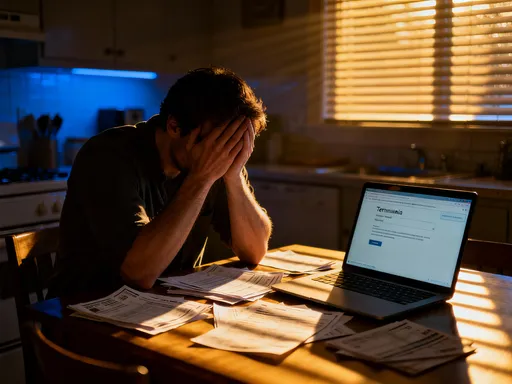

The Income Gap — Where the Money Really Vanishes

Perhaps the most underestimated factor in career switching is the income gap—the period between leaving one job and earning consistently in another. Even for those who plan meticulously, this gap tends to last longer than expected. Three months stretches to six. Six stretches to a year. During this time, living expenses don’t pause. Rent, utilities, groceries, insurance, and debt payments continue, creating pressure to dip into savings or take on debt.

This gap is dangerous not just because of what it costs, but because of how it alters financial behavior. When income stops, people start making trade-offs they never anticipated. They may take on gig work that drains energy but pays poorly, delaying progress in the new field. Others cut essential expenses, like health care or retirement contributions, creating long-term consequences. Some rely on credit cards to bridge the gap, only to find themselves trapped in high-interest debt once the transition is complete. The financial toll of the income gap is often greater than the sum of its parts.

Moreover, the timing of income recovery is unpredictable. Even after landing a new role, entry-level salaries in a new industry may be significantly lower than previous earnings. It can take years to regain the same income level, especially if the new field has a steeper learning curve or less demand. During this catch-up phase, lifestyle adjustments are inevitable. Families may need to downsize homes, delay vacations, or pause college savings. These changes, while practical, can create tension and stress, especially if partners or children don’t fully understand the long-term vision.

The psychological impact of inconsistent income also affects decision-making. When money is tight, people become more risk-averse in some areas and more impulsive in others. They might turn down networking opportunities due to cost, limiting their exposure, while simultaneously overspending on comfort purchases to cope with stress. This cycle undermines both financial stability and career momentum. The income gap, therefore, isn’t just a budgeting challenge—it’s a systemic threat to the entire transition process.

Benefits You Don’t Realize You’re Losing

Salary is only one part of total compensation, yet it’s the component most people focus on when evaluating a new opportunity. What’s often overlooked are the employer-sponsored benefits that quietly support financial well-being. Health insurance, retirement plan matching, paid time off, disability coverage, and stock options represent substantial value—value that disappears the moment employment ends. Replacing these independently is possible, but rarely affordable or as comprehensive.

Health insurance is perhaps the most immediate and costly loss. Employer plans typically cover a significant portion of premiums, sometimes up to 80%. When transitioning careers, especially into freelance or contract work, individuals must purchase coverage through the marketplace or private insurers, often at full cost. For a family of four, this can mean spending $1,000 or more per month—money that could otherwise go toward savings or debt reduction. Even with subsidies, the out-of-pocket costs for deductibles and prescriptions can be overwhelming, especially during periods of uncertainty.

Retirement contributions suffer doubly. Not only does the individual stop contributing during income gaps, but they also lose employer matching—a form of guaranteed return on investment. A 401(k) match of 5% on a $75,000 salary is $3,750 per year in free money. Over five years, that’s nearly $20,000 in missed growth, not including compound interest. Once back in the workforce, it takes years to rebuild that lost ground, especially if the new employer offers a less generous plan or none at all.

Paid leave, while intangible, has real financial value. The ability to take time off for illness, family needs, or personal development without losing income is a luxury many don’t appreciate until it’s gone. In a new career, especially in self-employment, every day without work is a day without pay. This pressure discourages rest, increases burnout risk, and limits long-term sustainability. Similarly, perks like tuition reimbursement, wellness programs, or commuter benefits vanish, forcing individuals to pay out of pocket for services they once received at little or no cost.

The Emotional Tax of Starting Over

The financial costs of a career change are measurable, but the emotional toll is just as real—and often more damaging. Starting over means facing constant self-doubt, isolation, and decision fatigue. You’re no longer the expert in the room. You’re the beginner, asking basic questions, making mistakes, and feeling invisible. This shift in status can erode confidence, especially for those who spent years building authority in their previous role.

Emotional strain doesn’t just affect mental health—it translates directly into financial decisions. When confidence is low, people are more likely to undervalue their services, accept underpaid gigs, or avoid negotiating for fair compensation. They may overspend on courses or coaching in hopes of a quick fix, believing that more training will finally make them “ready.” This cycle of self-doubt and overinvestment drains resources without guaranteeing results.

Isolation is another hidden cost. In a traditional job, you have colleagues, feedback, and a built-in support system. When transitioning, especially into independent work, that network disappears. Days can pass without meaningful interaction, leading to loneliness and decreased motivation. Some turn to therapy or coaching to cope, adding another expense. Others use shopping, dining out, or other forms of retail therapy to manage stress, further straining the budget.

Decision fatigue compounds the problem. Every day brings new choices: what course to take, which platform to use, how to price services, who to network with. Each decision requires research, time, and emotional energy. Over time, this constant evaluation wears people down, leading to procrastination or poor choices. The mental load of reinvention is exhausting, and when energy is low, financial discipline often suffers. The emotional tax, therefore, isn’t just a side effect—it’s a core driver of financial instability during career transitions.

Risky Bets People Make (and Regret Later)

When financial pressure mounts and progress stalls, people start taking risks they wouldn’t consider in stable times. One of the most common—and damaging—is dipping into retirement savings. Withdrawing from a 401(k) or IRA before age 59½ triggers taxes and a 10% penalty, eroding decades of growth. What feels like a short-term solution becomes a long-term setback, especially if the market is down or the transition takes longer than expected. Once that money is spent, it’s nearly impossible to recover.

Another frequent mistake is maxing out credit cards. Easy access to credit creates a false sense of financial security. People use cards to cover living expenses, certification fees, or business setup costs, assuming they’ll pay it off once the new income starts. But if the job search drags on or the new role pays less than expected, minimum payments become a permanent burden. High-interest debt can take years to clear, delaying other financial goals like homeownership or college savings.

Some rely on shaky side hustles to stay afloat—driving for ride-sharing apps, doing odd jobs, or selling personal belongings. While these can provide temporary relief, they often consume time and energy that should be spent building the new career. The result is a cycle of survival work that delays real progress. Others bet on unproven business ideas, investing savings into ventures with little market validation. Passion doesn’t guarantee demand, and many of these ventures fail, leaving individuals further behind.

Desperation leads to poor trade-offs. People accept roles that don’t align with their goals just to get a paycheck, only to feel trapped again. They neglect their health to save money, risking long-term consequences. They borrow from family, straining relationships. These choices, made under pressure, often lead to regret. The lesson isn’t that risk should be avoided entirely, but that it should be calculated—not driven by fear or urgency.

Building a Smarter Transition Plan

A successful career change doesn’t have to be a financial disaster. With careful planning, it’s possible to minimize risk and maintain stability. The key is preparation over inspiration. Start by building a financial buffer—ideally six to twelve months of living expenses—before making any move. This cushion provides breathing room, reducing the pressure to accept the first available opportunity.

Next, conduct a thorough expense audit. List every potential cost of the transition: certifications, technology, insurance, coaching, marketing materials. Research actual prices and build a realistic budget. Include a 20% contingency for unexpected expenses. At the same time, evaluate the value of current benefits and calculate what it would cost to replace them independently. This creates a clearer picture of the true financial gap.

Test the new path before fully committing. If possible, explore the field part-time while still employed. Take online courses, volunteer, or freelance on weekends. This allows you to validate interest, build skills, and even generate early income without quitting. It also helps establish a network and gain references before the leap.

Emotional safeguards are just as important. Identify sources of support—mentors, coaches, peer groups—who can offer guidance and encouragement. Set realistic milestones and celebrate small wins to maintain motivation. Practice self-compassion; setbacks are part of the process, not proof of failure. And above all, maintain routines that support mental and physical health, even when time and money are tight.

Conclusion

A career shift isn’t just a change of job—it’s a financial rebalancing act with no safety net. The real cost isn’t just what you spend, but what you lose before you even notice. From hidden fees to lost benefits, from income gaps to emotional strain, the journey demands more than courage. It requires clarity, planning, and a deep understanding of both visible and invisible expenses. By seeing the full picture, you can move forward not just with hope, but with strategy. The dream of reinvention is worth pursuing, but it’s safest when built on a foundation of financial awareness and emotional resilience. When you know the true cost, you’re not just taking a leap—you’re making a calculated move toward a more sustainable future.